You click "withdraw" on your crypto app, expecting the Naira to hit your bank account within minutes. Instead, you get a notification that your transaction is pending, or worse, your account is frozen. If you are trading cryptocurrency in Nigeria today, this anxiety is familiar. The landscape has shifted dramatically from the outright bans of the past to a complex, heavily regulated environment in 2026.

So, how do banks actually react when you move money from crypto to fiat? The short answer is: it depends entirely on where you withdrew from and whether your bank sees red flags. Since the Central Bank of Nigeria (CBN) lifted its ban in late 2023 and the Investments and Securities Act 2025 (ISA 2025) came into force, the rules are clear on paper but strict in practice. Banks are no longer blocking all crypto transactions, but they are acting as gatekeepers for compliance. Understanding their reaction requires knowing the difference between a smooth transfer from a licensed exchange and a frozen account linked to peer-to-peer (P2P) risks.

The Shift from Ban to Conditional Acceptance

To understand why your bank might hesitate, you have to look at where we started. For nearly three years, starting in February 2021, the Central Bank of Nigeria (CBN) imposed a strict ban on commercial banks processing any cryptocurrency transactions. This forced traders into the shadows, relying on informal channels and P2P marketplaces. By 2022, despite the ban, Nigeria was already the second-largest country globally for P2P trading volume. The pressure was too high to ignore.

The turning point came on December 22, 2023, when the CBN issued new guidelines allowing banks to open accounts for Virtual Asset Service Providers (VASPs). Then, in March 2025, President Bola Ahmed Tinubu signed the Investments and Securities Act 2025 (ISA 2025), which officially recognized digital assets as securities under Nigerian law. This placed oversight responsibility squarely on the Securities and Exchange Commission (SEC).

However, legalization did not mean deregulation. Banks reacted by implementing what they call "prudent" controls. They can now process withdrawals, but only under specific conditions. If you are using an unlicensed platform, the bank’s reaction will likely be negative. If you are using an SEC-approved exchange, the reaction should be neutral to positive, provided you follow the rules.

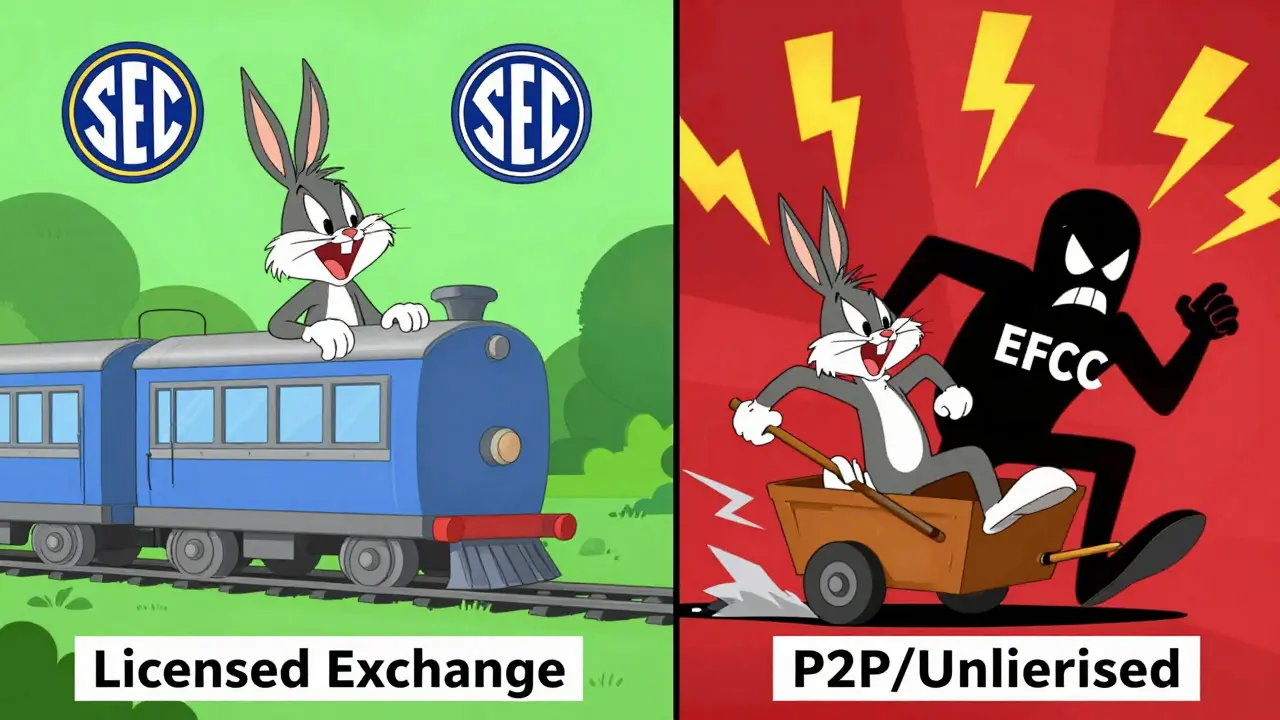

Licensed vs. Unlicensed Exchanges: The Two-Tier System

This is the most critical factor in how your bank reacts. There is now a distinct two-tier system in Nigeria’s crypto banking sector.

Tier 1: Licensed Exchanges

Platforms like Luno and other SEC-licensed entities operate with regulatory backing. When you withdraw Naira from these platforms, the bank sees a legitimate electronic transfer from a registered financial service provider. These transactions typically process within a few hours. The bank applies standard Anti-Money Laundering (AML) checks, but unless your behavior is erratic, the money arrives without issue. Fees apply, but the friction is low.

Tier 2: Unlicensed Platforms and P2P

This is where the danger lies. Many Nigerians still use major international platforms that do not hold local licenses or engage in direct P2P trades. Here, banks view incoming funds with extreme suspicion. If you receive Naira from an individual buyer via P2P, the bank does not see a clean corporate transfer. It sees a personal transfer that may be linked to illicit activities. This triggers enhanced scrutiny, potential holds, or even account closures.

| Factor | Licensed Exchange (e.g., Luno) | Unlicensed/P2P Trading |

|---|---|---|

| Transaction Speed | Fast (few hours) | Delayed or Blocked |

| Bank Scrutiny Level | Standard AML/KYC | Enhanced Due Diligence |

| Risk of Freeze | Low | High |

| Cash Withdrawal Allowed? | No (Electronic only) | No (Electronic only) |

| Regulatory Protection | Yes (SEC Oversight) | No |

The Ghost of Account Freezes: EFCC Enforcement

You cannot discuss bank reactions without mentioning the Economic and Financial Crimes Commission (EFCC). Even though crypto is legal, the authorities are aggressive against suspected market manipulation or money laundering. Banks are required to cooperate fully with EFCC investigations.

A stark example occurred in September 2024, when the EFCC secured court orders to freeze 22 bank accounts belonging to USDT sellers on platforms like Bybit and KuCoin. The frozen amount totaled approximately ₦548.6 million. The allegation? Manipulating the Naira exchange rate. This sent a shockwave through the community. It proved that even if you believe your trade is legitimate, if the source of the Naira is tainted, the bank will freeze your account immediately upon instruction from regulators.

Banks act as de facto gatekeepers. They monitor transaction patterns, volumes, and frequencies. If you suddenly start receiving large sums from multiple unknown individuals-typical of high-volume P2P selling-the bank’s automated systems flag this as suspicious. The result is often a temporary freeze while the bank conducts due diligence, or a permanent closure if they deem the risk too high.

Transaction Limits and Cash Restrictions

Even if you are doing everything right, you will notice constraints. Under the current guidelines, banks impose mandatory transaction limits on crypto-related accounts. These limits are described as "prudent" but are rarely publicized. They vary by bank and account type, often being significantly lower than limits for traditional salary or business accounts.

Furthermore, there is a hard rule: no cash withdrawals from crypto accounts. All transactions must go through electronic banking channels. You cannot withdraw Naira from a crypto-linked account and take physical cash from an ATM or teller window. This restriction is designed to create a digital trail for AML purposes. Attempting to bypass this by transferring to another account just to withdraw cash can trigger additional scrutiny.

Taxation and Future Compliance

As of 2026, the tax landscape is evolving. The Federal Inland Revenue Service (FIRS) has stated that cryptocurrency transactions are taxable as capital gains. While specific crypto tax laws were still being refined through proposed Finance Bills, the intent is clear: align with international norms. Banks may soon be required to report large or frequent crypto-to-fiat withdrawals to tax authorities.

This means that withdrawing substantial amounts regularly could lead to documentation requests from your bank. They may ask for proof of the source of funds to ensure you are compliant with tax obligations. Keeping detailed records of your trades, profits, and tax payments is no longer optional; it is essential for maintaining a healthy banking relationship.

Best Practices for Smooth Withdrawals

If you want your bank to react positively-or at least neutrally-to your crypto withdrawals, follow these steps:

- Stick to SEC-Licensed Exchanges: Use platforms like Luno that are approved by the SEC. This provides a layer of regulatory legitimacy that banks respect.

- Maintain Consistent Patterns: Avoid sudden spikes in transaction volume. If you usually withdraw ₦50,000 a month, don’t suddenly withdraw ₦5 million without prior communication with your bank.

- Complete Full KYC: Ensure both your crypto exchange profile and your bank account are fully verified with matching identification documents.

- Avoid High-Risk P2P: If you must use P2P, be extremely cautious about who you trade with. One bad actor sending dirty money can ruin your banking history.

- Diversify Banking Relationships: Do not rely on a single bank. Having accounts with different institutions, including fintech-oriented banks that are generally more crypto-friendly, reduces the risk of total access loss if one bank freezes your account.

- Keep Records: Save every transaction receipt, trade history, and correspondence. If your account is frozen, evidence of legitimate activity is your best defense.

Conclusion: Navigating the Gray Area

Nigeria’s crypto banking environment is a work in progress. The days of total prohibition are over, replaced by a regime of strict oversight. Banks are not enemies, but they are risk-averse institutions following tight regulatory mandates from the CBN, SEC, and EFCC. Their reaction to your withdrawal depends on your compliance. Use licensed platforms, keep your transactions transparent, and respect the limits. By doing so, you can navigate the system safely and convert your crypto to Naira without fear of losing access to your finances.

Can I withdraw crypto to my Nigerian bank account directly?

Yes, but only if you withdraw from an SEC-licensed exchange like Luno. Direct withdrawals from unlicensed platforms or P2P trades may be blocked or frozen by banks due to compliance risks.

Why did my bank freeze my account after a crypto withdrawal?

Banks freeze accounts if they detect suspicious activity, such as receiving funds from unverified sources or engaging in high-volume P2P trading that resembles money laundering. The EFCC may also instruct banks to freeze accounts involved in alleged market manipulation.

Is it legal to trade crypto in Nigeria in 2026?

Yes. The Investments and Securities Act 2025 (ISA 2025) legalized digital assets as securities. However, you must use licensed platforms and comply with AML/KYC regulations to avoid legal issues.

Can I withdraw cash from my bank account after receiving crypto proceeds?

No. Current guidelines prohibit cash withdrawals from accounts linked to crypto transactions. All transfers must remain within electronic banking channels to maintain a clear audit trail.

Which banks are most crypto-friendly in Nigeria?

Fintech-oriented banks and digital banking platforms tend to be more crypto-friendly than traditional commercial banks. However, policies change frequently, so it is best to check with your specific bank regarding their current stance on crypto-related transactions.

Are crypto transactions taxed in Nigeria?

Yes, the Federal Inland Revenue Service treats crypto transactions as taxable capital gains. Be prepared to provide documentation for large withdrawals to prove tax compliance.

What happens if I use Binance or Bybit in Nigeria?

Using unlicensed international platforms carries higher risk. Authorities have cracked down on these platforms, and banks may block transactions or freeze accounts associated with them due to lack of local regulatory oversight.